BRICS Lays First Tracks for New Global Payment System to Challenge Dollar-centric Networks.

A digital currency substitute for SWIFT is almost here, but a BRICS currency to aid with de-dollarization is still a long way off.

A payment mechanism connecting national digital currencies will be the main focus as India gets ready to host the BRICS summit later this year. The bloc takes a practical wager that workable mechanisms will transform global banking more than token gestures by putting this infrastructure ahead of the introduction of a new currency. Creating a BRICS payment system based on interoperable central bank digital currencies (CBDCs) is a key agenda item for the summit that suggests a possible change.

Italian PM Meloni and PM Modi's Video Shared by Melodi Team

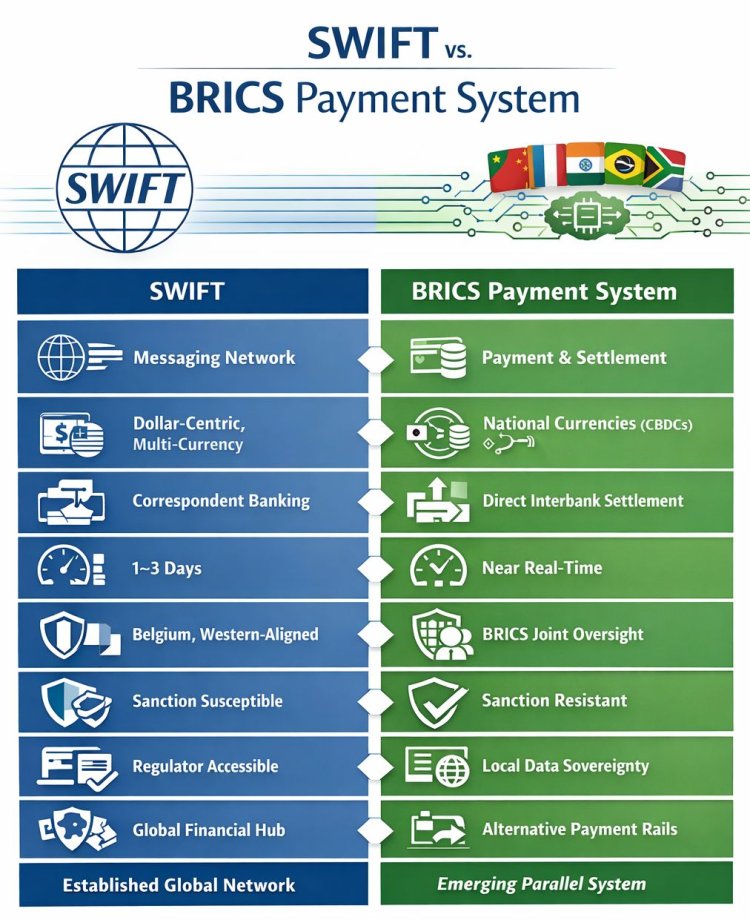

Because it avoids the drama of requests for a "BRICS currency" or overt de-dollarization, this infrastructure-focused plan has received less attention. Its avoidance of attention-grabbing actions, however, may make it more significant, highlighting the central claim that real infrastructure improvements have the power to transform finance more than symbolic obstacles. In keeping with this, the proposal concentrates on a more practical strategy—constructing alternative payment rails that enable commerce to be settled directly across national digital currencies, lowering reliance on the dollar-based SWIFT system—rather than directly opposing the dollar.

Not a currency

There is a persistent misconception about BRICS financial cooperation. The current plan does not call for member states to give up their monetary sovereignty to a supranational body, nor does it aim to establish a common BRICS currency.

Previous ideas along such lines failed for expected reasons: concerns about the supremacy of the Chinese yuan, incompatible capital controls, and differing inflation regimes. The current strategy takes a different approach. Through interoperable infrastructure, it seeks to connect current national CBDCs, such as the digital rupee of India, the digital yuan of China, and the digital ruble of Russia.

Every currency maintains its complete sovereignty. The infrastructure that makes it possible for them to communicate more effectively is what changes.

US deflects very first default, endorses obligation limit suspension

Practically speaking, this would allow cross-border payments to be settled directly in national currencies, bypassing the dollar-centric SWIFT network and correspondent institutions. The appeal to participants is obvious: quicker settlement, less transaction fees, and less vulnerability to Western governments' asset freezes or sanctions.

India’s central role

India plays a crucial role. New Delhi has advanced CBDC interoperability from a theoretical debate to practical policy cooperation in its capacity as the summit's host and agenda-setter.

The success of India's Unified Payments Interface (UPI) at home has informed the country's broader digital payments ideology, which emphasises interoperability and maintaining monetary sovereignty.

The digital rupee is not a crypto-asset and is not a step toward a currency union, according to the Reserve Bank of India, which is crucial to the process. It is a digital currency backed by the state that aims to increase productivity while maintaining governmental control.

Myanmar earthquake: India will deploy 80 NDRF members under "Operation Brahma."

This position explains why India has supported infrastructure that increases the usability of national currencies in cross-border trade while opposing ideas for a supranational BRICS currency. Another factor has been experience.

The "rupee trap" refers to the situation where Moscow held substantial sums of rupees that were difficult for it to spend as a result of previous bilateral settlement agreements with Russia. The necessity for a global network where earned currencies can move throughout a larger trading bloc instead of accumulating pointlessly was highlighted by that failure.

Direct settlement

Settlement cycles and foreign exchange swap lines, two crucial systems intended to facilitate trading in national currencies without depending on the dollar, are at the core of the proposed new BRICS payment system.

A periodic netting system is provided by settlement cycles. All payments between two nations are accumulated over a predetermined length of time rather than requiring an instantaneous exchange for each transaction, which necessitates continuous, huge currency liquidity. Only the net difference is decided at the conclusion of the cycle.

For instance, only the net ₹100 billion that India owes China must be transferred if Chinese imports from India total ₹400 billion and Indian imports from China total ₹500 billion in a given month.

This significantly lowers the amount of money that needs to be physically transported, which lowers expenses and removes the possibility that one nation will have a big, useless excess of another's currency. A safety net for liquidity is provided by forex swap lines.

In a US plane crash, a woman of Indian descent died and her daughter suffered severe burns.

These are agreements made in advance between central banks to swap certain sums of their respective currencies for a predetermined duration of time.

Dollar debt concerns

The dollar, the cornerstone of contemporary international banking, cannot be replaced by the BRICS system in any way. Approximately 59% of the world's foreign exchange reserves, 58% of international payments, and more than half of all cross-border transactions are invoiced in dollars.

At the same time, one of the main causes of systemic financial risk is the enormous amount of debt denominated in US and international dollars. The worldwide debt is estimated to be $315 trillion, of which 64% is denominated in dollars, and the US national debt is close to $39 trillion. As a result, maintaining confidence in the dollar is crucial to the stability of the global economy.

A self-reinforcing cycle is the main issue. The ongoing demand for dollar assets, mainly US Treasury bonds, around the world is necessary to service the enormous US debt. Interest rates may spike if this demand falters as a result of US policy or geopolitical changes.

31 children who fled Russia for Ukraine have returned home amid the conflict.

In addition to tightening global financial conditions, higher rates would significantly raise the US government's debt servicing expenditures, which are currently the largest item in the federal budget. This can lead to defaults and problems among other countries and businesses that have dollar loans. The US and the rest of the world that depends on dollar liquidity would be vulnerable as a result of this dynamic.

US defensive actions

Instead than depending on any one dramatic action, the United States uses a multifaceted strategy that combines institutional, financial, and occasionally coercive measures to defend the dollar in its role as the primary global reserve currency. Financial sanctions and access to the dollar-centric global payment system SWIFT are two main deterrents.

As an example of the tremendous cost of trying to operate outside of the dollar ecosystem, nations like Iran and Russia have experienced significant economic isolation for opposing US objectives. Because "de-dollarization" initiatives run the risk of isolating countries from the biggest financial market and most traded currency in the world, this presents a strong deterrent for others.

At the same time, the US is attempting to modernise and broaden the dollar's appeal. Digital finance is the most important new area. The framework for dollar-denominated stablecoins—cryptocurrencies linked to the US dollar—is being actively shaped by US financial institutions and authorities. The objective is to solidify the dollar's dominance in the quickly developing digital economy by guaranteeing that these digital assets function under US regulatory supervision, appropriating innovation rather than being upended by it.

US Treasury Chief: Oil Tariffs Will Collapse Russian Economy

However, central bankers and investors are concerned about recent patterns. The growing demand for gold among central banks around the world is a crucial indicator. For the first time in almost thirty years, foreign central banks' combined gold holdings exceeded their US Treasury holdings in terms of value in 2025. Gold's sharp price increase, which increased by 60–70% in 2025 and sent prices well above $4,000 per ounce for the first time in history, highlighted this historic crossover. In the first month of 2026, prices have continued to soar, reaching almost $5,500 per ounce.

Without completely upending the existing monetary order, this progressive rebalancing toward "neutral" assets like gold—one of the few that has no counterparty risk when the owner has physical possession—improves resilience. However, it draws attention to the declining trust in an excessively dollar-centric economy.

There is still much disagreement about whether the US can arrange a "soft landing" for its debt load through controlled inflation. To do this, the debt would need to be inflated away without causing the economy to collapse. However, most Americans' living standards would decline as the dollar's purchase power declined.

Shock absorber

The BRICS's repeated efforts to create a parallel payment line alongside SWIFT can be partially explained by concerns about the dollar. The theft of $300 billion in Russian reserves and Russia's exclusion from the SWIFT system were additional issues. Iran, North Korea, and Cuba also had their assets frozen or seized, so Russia was not the only nation to suffer from the fury of the Western financial system. However, Russia turned into a turning point. No nation is exempt from suffering the same fate if Russian assets may be frozen.

8-year-old girl smiles as she demands money from Putin for her native country

To be sure, there are still a lot of obstacles to overcome before BRICS has a fully functional payment rail that can replace SWIFT, including technological implementation and legal harmonisation.

The majority of BRICS countries' CBDCs are still in the testing phase (the digital ruble, digital rupee, and e-CNY have not yet reached full scale), and interoperability is beset by governance, regulatory, and technical issues. However, an alternative banking system is now an economic and financial need due to the unpredictability of US actions and the escalating geopolitical and geoeconomic conflicts. In the event of a global crisis, the BRICS payment system might offer a another payment channel by creating a parallel payment rail. It would keep cross-border trade from coming to a total standstill and enable vital transactions, especially in commodities and energy.

A BRICS payment rail might prevent contagion, buy time for a concerted policy response, and enable a more controlled, less disastrous transition to a new financial equilibrium by guaranteeing ongoing transactional functionality for a sizable chunk of the world economy.

Laying the rails

Before growing into a multilateral network, the development of BRICS payment rails is probably going to proceed pragmatically, utilising current bilateral systems. As an illustration, consider the fundamental connection between India and six other nations as well as the UAE, a significant BRICS-related economy.

The UAE's Instant Payment Platform (IPP) and India's Unified Payments Interface are already compatible, enabling quick and inexpensive cross-border payments. Other BRICS partners can use this established corridor as a tried-and-true model and technical guide. The integration of other members with strong domestic instant payment systems, like Brazil's PIX or possibly China's CIPS/digital yuan infrastructure, would be the obvious focus of expansion.

Developing a central hub or common communications standard that links these disparate national systems without necessitating total harmonisation will be the difficult part. This first manifests as a web of bilateral agreements that directly lessen reliance on the Western-centric SWIFT for local currency transaction payments.

A single BRICS platform that enables direct transactions in member currencies is the long-term goal. It is entirely voluntary to participate. Overcoming geopolitical differences and harmonising technical standards are essential for success.

The direction of movement is sufficiently obvious to merit attention, even in the face of substantial obstacles. A different course is practically a historical necessity, but the era of a single hegemonic financial system is not coming to an end overnight. The first rails are being laid by BRICS, with India leading the way.

Former PM Imran Khan is granted bail by a Pakistani anti-terrorism court.